Key Terms

- CBAM certificate

- An electronic certificate corresponding to one tonne of CO2 equivalent of embedded emissions in imported goods, purchased at a price linked to the EU ETS allowance price [Art. 3(24)].

- Authorised CBAM declarant

- A person authorised by a national competent authority to import CBAM goods into the EU customs territory and to submit CBAM declarations [Art. 3(17), Art. 17].

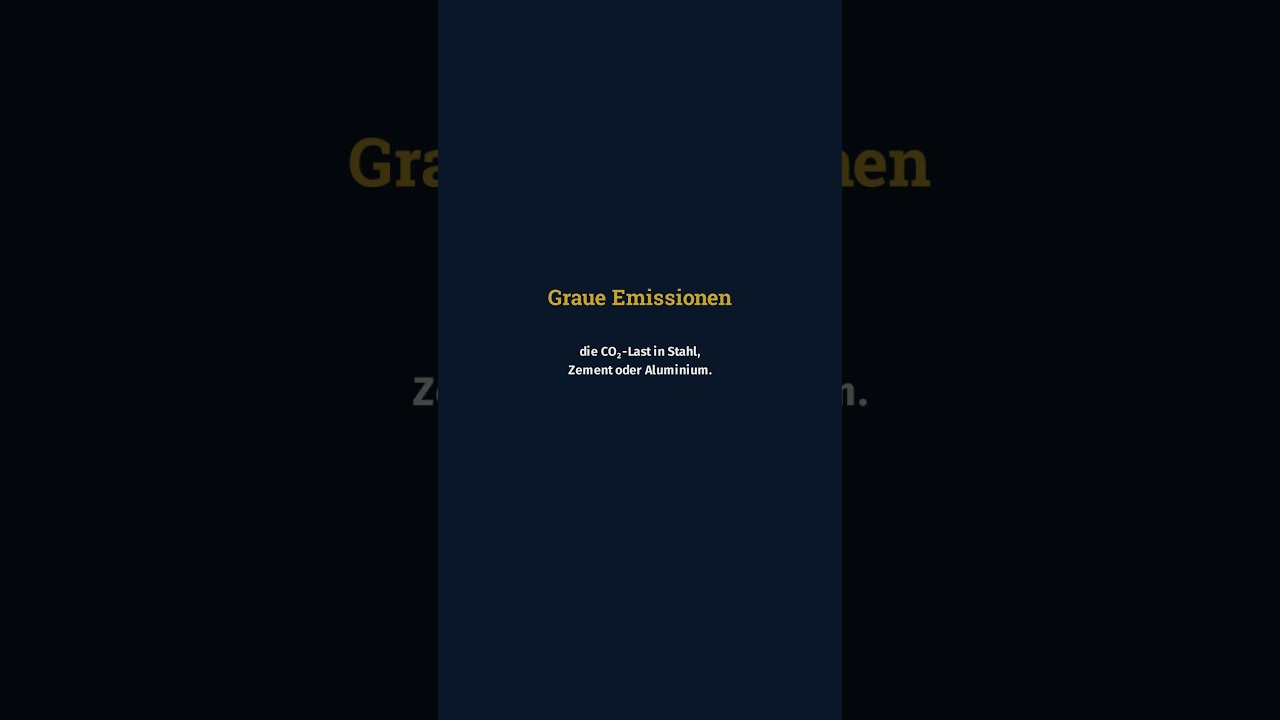

- Embedded emissions

- Direct emissions released during the production of goods and indirect emissions from electricity consumed in those production processes, calculated pursuant to Annex IV [Art. 3(22)].

- Carbon leakage

- The risk that production — and its associated greenhouse gas emissions — relocates from the EU to third countries with less ambitious climate policies, undermining overall emission reductions.

- EU ETS (EU Emissions Trading System)

- The EU system for trading greenhouse gas emission allowances among installations in the EU, to which CBAM certificate pricing is aligned [Art. 3(5), Art. 21].

- Default values

- Values calculated or drawn from secondary data representing the embedded emissions in goods, applied when actual installation-level data is not available [Art. 3(27), Annex IV point 4.1].

- CBAM registry

- A standardised EU electronic database managed by the Commission containing data on authorised CBAM declarants, their certificates, third-country operators and accredited verifiers [Art. 14].

Frequently Asked Questions

Which goods are covered by CBAM?

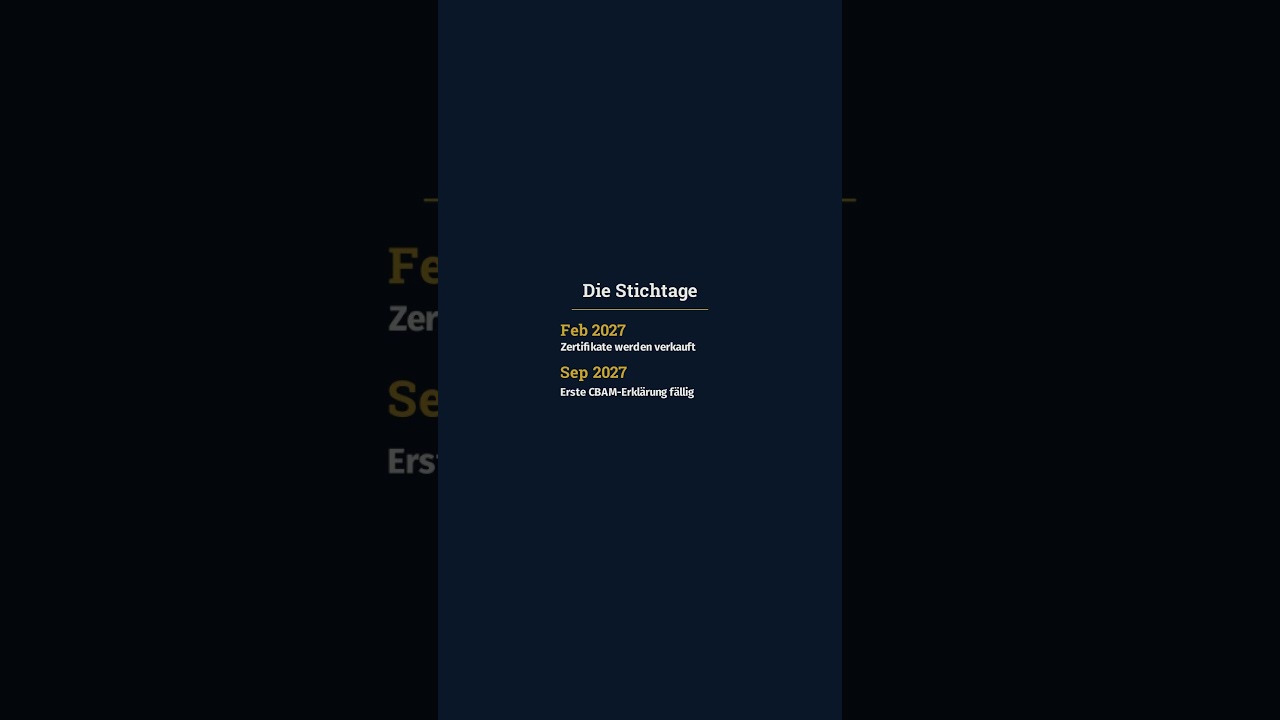

What is the transitional period and what obligations applied during it?

How is the price of a CBAM certificate determined?

Can the carbon price paid in the country of origin be deducted?

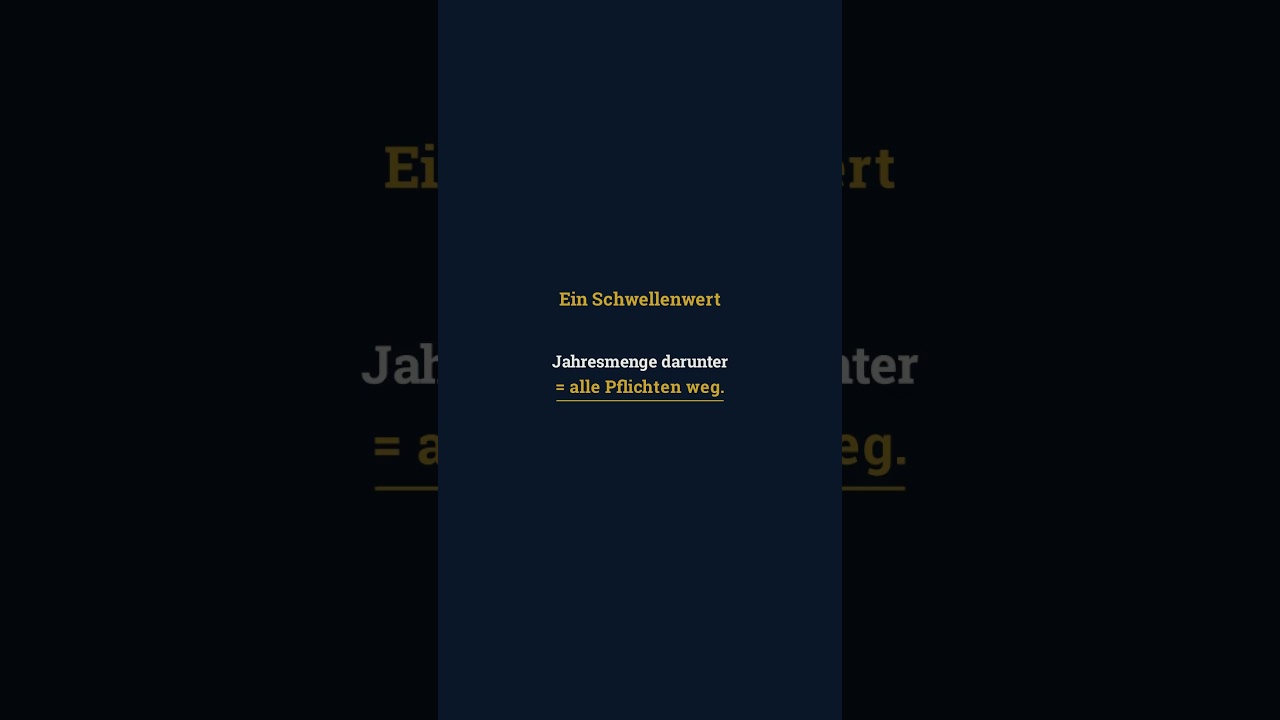

What is the de minimis exemption introduced by Regulation (EU) 2025/2083?

What happens if an importer does not have authorised CBAM declarant status?

How are embedded emissions calculated?

Assessment Factors & Checklist

PremiumQuestions for Your Lawyer

PremiumConclusion & Summary

PremiumDetailed analysis with source links.

Schalten Sie die KI-Analyse frei — mit markierten Fundstellen und direkten Links zu EUR-Lex. Kostenlos prüfen mit Scout.

Keine Kreditkarte. 50 Recherchen + 5 KI-Analysen frei.

In short — videos on this topic

60-second explainers from our YouTube channel. Click opens YouTube in a new tab — no YouTube embed, no tracking on this page.

0:54Opens YouTube

0:54Opens YouTube 0:43

0:43Im Ausland schon CO₂ bezahlt — an der Grenze nochmal? (Art. 9) #compliance #cbam #co2reduction

Opens YouTube 0:51

0:51Stahl importiert — zahlen Sie für mehr CO₂ als nötig? (CBAM, Art. 7) #compliance #cbam #import

Opens YouTube 0:47Opens YouTube

0:47Opens YouTube 0:51

0:51Alles bezahlt - und am Zoll fehlt trotzdem etwas (CBAM, Art. 4) #compliance #cbam #eucompliance

Opens YouTube 0:43

0:43Den Preis bestimmen nicht Sie — sondern ... (CBAM, Art. 21) #compliance #cbam #carbonemissions

Opens YouTube 0:40

0:40Importmenge zu klein für die Pflicht? Diese Grenze hat eine Falle (CBAM Art. 2a) #compliance #cbam

Opens YouTube